You’re On the Clock, Part Four: Eat the Dead Cap

Making the hard call when your benefits strategy isn’t delivering.

The Super Bowl is this weekend, but for most NFL teams, the season is already over. Thirty teams are out. Their focus has shifted from winning games to building next year’s roster.

That means making hard decisions. Which players stay. Which ones go. Which expensive contracts get restructured or cut entirely, even if it means paying players who won’t be on the team.

The cost of paying out a player’s contract after you’ve released them or traded them at a discount is called dead cap money. From fans to the front office, everyone universally hates it. Paying millions to players who aren’t contributing feels like pure waste.

It’s painful, but teams do it all the time. Why? Because keeping the wrong player in place costs even more.

A lesson from the Denver Broncos

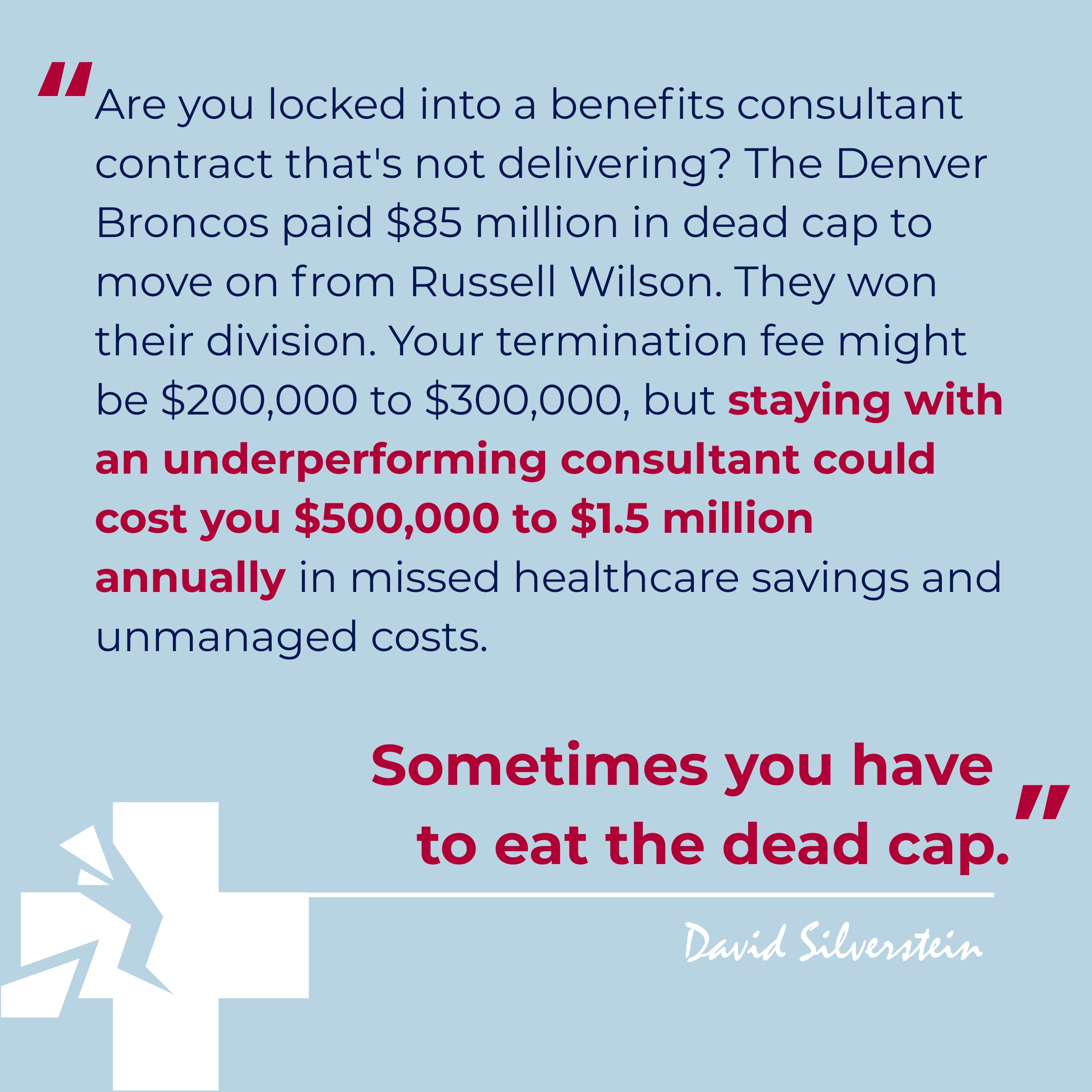

The Denver Broncos paid Russell Wilson $53 million in 2024 and another $32 million in 2025 even though he left the team at the end of the 2023 season. That’s $85 million in dead money for a quarterback who wasn’t even on their roster.

In 2024, the NFL salary cap was $255.4 million. Denver’s $53 million dead cap payment that year represented more than 20% of their total cap, an enormous number by any standard.

They did it anyway, and they are [clearly] better for it. This season, the Broncos won their first division title in a decade.

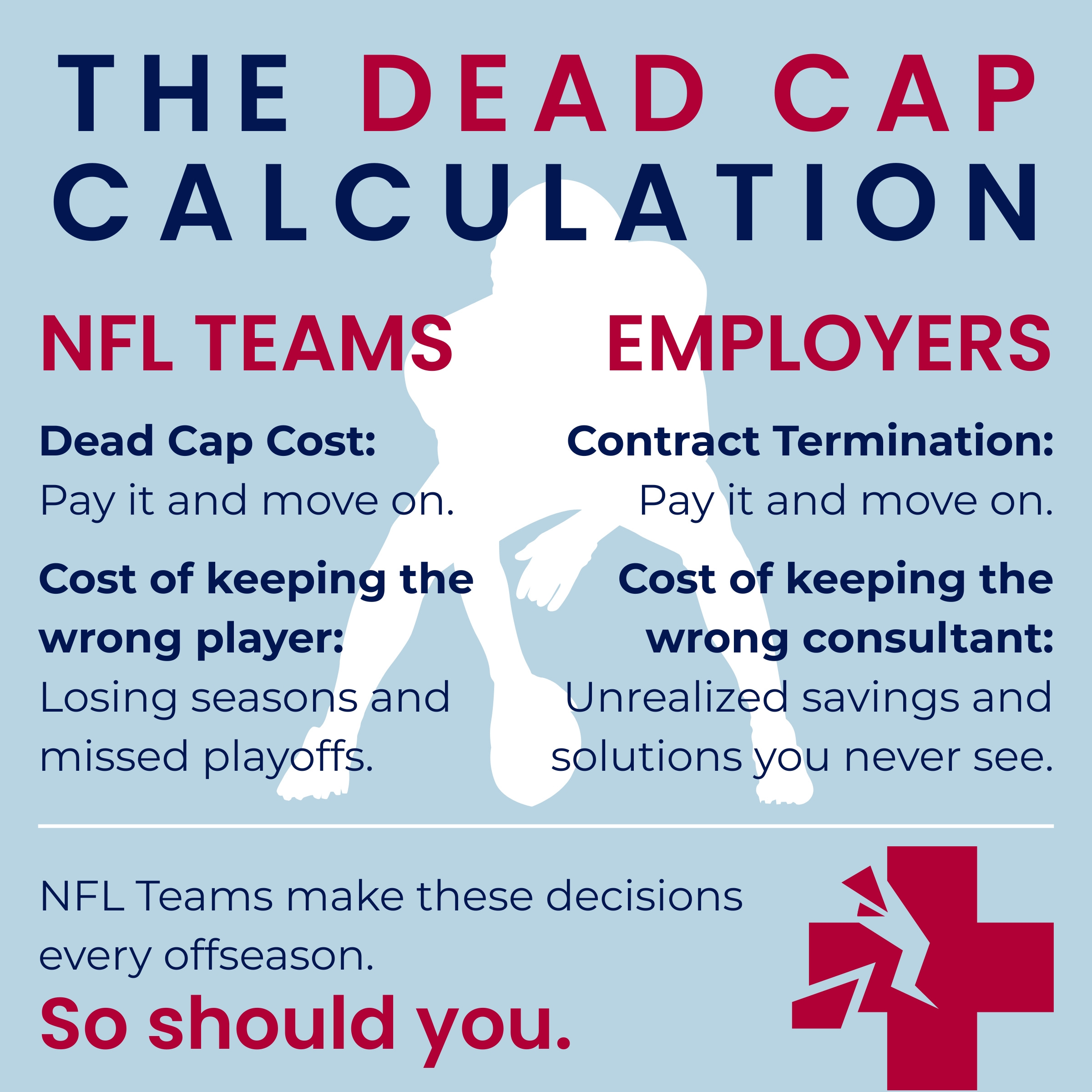

Your dead cap problem

Many companies are facing the same decision with their benefits broker or consultant. They’re locked into multi-year contracts that felt reasonable when they were signed. At the time, the relationship worked or worked well enough. Now, the relationship isn’t delivering, but breaking the contract feels expensive enough to justify staying the course for another year.

If this feels familiar to you, don’t let the wrong question start driving your decision.

The first question to ask isn’t “What will it cost to release the current firm?” It’s “What will it cost not to?”

Consultant fees typically show up as a fixed amount (say, $500K annually) or a PEPM (per employee per month) structure. As a general rule, if that number exceeds 5% of your healthcare spend, you’re overpaying. Even at 10%, the upper limit for smaller companies, eating the cost could still make financial sense.

The more expensive mistake

The termination fee is easy to see. It’s right there in your contract. The cost of maintaining the relationship isn’t. It’s spread across renewals, pharmacy spend, vendor contracts, and missed opportunities over the next two to three years. And it’s often much larger.

Not every dollar of healthcare inflation is controllable; experienced HR leaders know that. But some of it is structural, and that’s where underperforming relationships compound.

That $1,000 to $3,000 per employee we’ve mentioned throughout this series? It compounds every year. For a company with 500 employees, that’s $500,000 to $1.5 million annually in missed savings, inefficiencies, and unmanaged risk.

Your dead cap payment might be $200,000 or $300,000. Painful? Absolutely. But compare that to ongoing annual costs in the six, seven and eight-figure range. In many cases, one more year with an underperforming consultant can cost more than several years of dead cap payments.

That’s a calculation most employers never sit down and do.

When to walk away

Sometimes, you have to eat the dead money.

None of this means you should fire your broker tomorrow. But the cost to break your contract is not a valid reason to delay change when the relationship isn’t working.”

If your consultant hasn’t brought you solutions that other employers are already using—alternative insurance models, modern pharmacy strategies, accountable vendor approaches—staying means more years of rising costs with nothing to show for it.

At some point, you have to decide whether you’re paying for continuity or paying for progress.

NFL teams make their biggest roster decisions in the offseason because waiting until the season starts limits their options. The same is true here.

Your renewal will arrive in September whether you’re ready or not. You need to decide whether you’ll let the fear of dead cap money keep you stuck for another year with a consultant who isn’t delivering.

Championship teams don’t cling to sunk costs when better options exist. Neither should you.

You’re on the clock.

If you haven’t already, read the entire series of ‘You’re On the Clock’ and share it with an HR leader who could benefit from it:

Part 1: The Draft for Your Next Benefits Broker Starts Now

Part 2: Are You Ready to Draft a Franchise Broker?

Part 3: The Blitz Is Coming