What Your Benefits Consultant Isn’t Telling You About Their Paycheck

A look inside the hidden world of employee benefit consultant compensation.

Are you paying more for healthcare than you should because of how your advisor gets paid?

Most employers would say no. After all, you hired a benefits consultant; they quoted you a flat fee or a per-employee-per-month rate, and you signed the contract knowing exactly what you’re paying.

Or do you?

Odds are, you don’t.

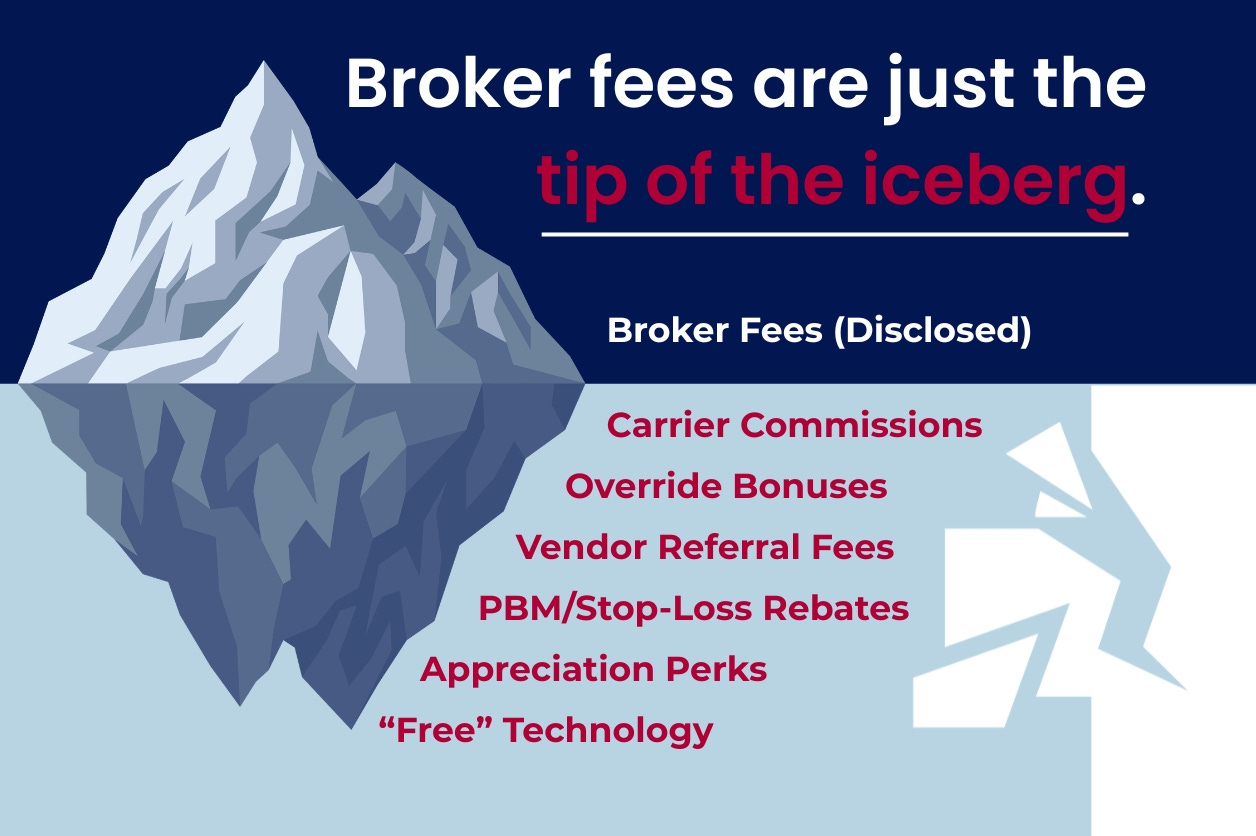

For consultants who work on commission or hybrid models, the fees disclosed in your contract are just the tip of the iceberg. Behind them sits a network of payments, bonuses, and perks that many employers never see. This is where significant money often flows, and it can push up both your costs and those of your employees. The wrong design of your plan can also tie your hands, preventing you (or your employees) from controlling costs as you’d like.

If you’re signing off on benefits decisions, you need to know your consultant’s full compensation structure, not just to control costs, but to make sure the advice you’re getting serves your interests and to stay on the right side of your fiduciary obligations to your employees.

Commissions built into premiums

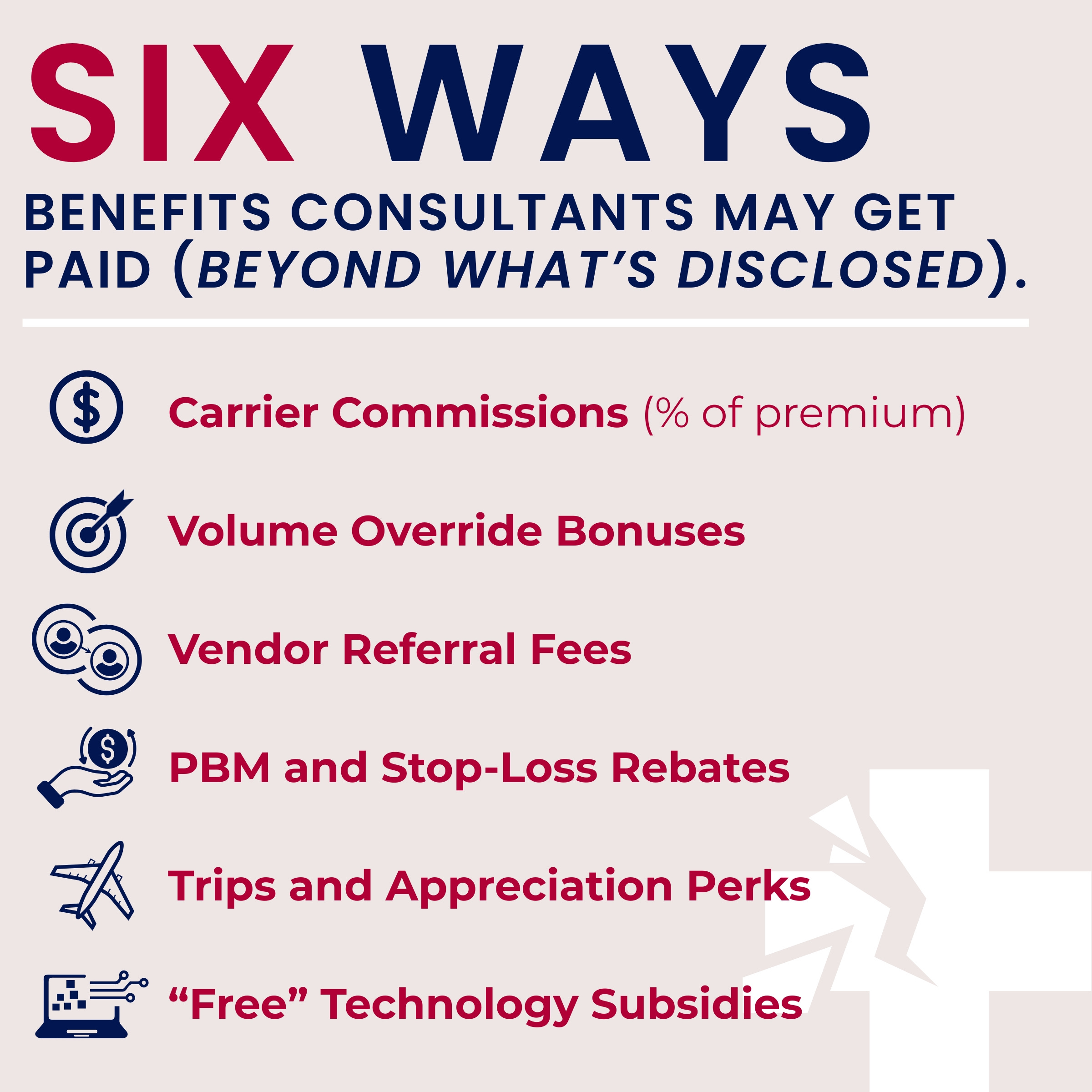

Some employee benefit consultants supposedly work on a “fully transparent,” fixed fee basis, forgoing commissions for the very purpose of telling you that’s exactly what they do. But did you know they often receive bonuses (not commissions ) for hitting key milestones such as securing your renewal or bringing in a certain number of new customers?

They are supposed to provide you with an estimate of these bonuses, and they are supposed to update you as those estimates change. When was the last time you saw such an estimate?

And then there are the other products you offer to your employees. Do you know what commissions your broker earns on the voluntary benefits they sell to your employees? Those would be your vision plan, dental plan, critical illness or accident indemnity plan, among others. By creating the façade of transparency on your medical plan, you open the door to all kinds of other abuse.

Overrides and retention bonuses

For commission-based consultants, standard commissions are just the start. Many carriers also pay overrides. These are bonus payments for bringing in new business or keeping existing clients from switching. However, these bonuses aren’t based on your account alone; they can be tied to a consultant’s total volume across their entire book of business with a carrier. That empowers your broker to rationalize why it’s none of your business. But, of course, it is.

Here’s what makes overrides particularly problematic: they are often all-or-nothing. If a consultant needs to write a certain amount of new business or keep a certain percentage of clients renewing, and they fall short, the entire bonus disappears. Your renewal might be the account that pushes them over the threshold or causes them to miss it.

That can create real pressure to keep you with certain carriers, even when switching would save you money or get you better coverage. These payments can be substantial, sometimes rivaling or exceeding the base commission, and they pay month after month as long as the consultant maintains their volume targets.

These numbers seldom appear in proposals or contracts, but they help explain why the same carriers keep showing up at renewal, year after year.

Point solution vendor fees

Mental health platforms; diabetes programs; wellness apps... the list goes on. The point solution market has exploded, and many vendors pay consultants to get in front of employers.

Each time a consultant introduces a new tool, they may receive referral fees, marketing allowances, or a per-employee placement bonus. The pitch sounds good—this platform will fill a gap in your plan, engage your employees, and improve outcomes, but what you don’t see is the check the vendor writes to your consultant for making that introduction.

The next year, there’s often a different vendor solving the same problem with a new tool and a new payment. They’ll call it innovation or staying current with best practices. What it really creates is churn: a rotation of vendors that generates fees without necessarily improving your employees’ experience or your plan’s performance.

Without full disclosure, you have no way to know whether a recommendation is driven by what your population needs or by what the vendor is willing to pay.

Pharmacy and stop-loss rebates

If you’re self-funded, there may be additional layers. Some consultants collect rebates from pharmacy benefit managers, stop-loss carriers, or both.

PBMs may pay consultants through rebates, administrative allowances, or performance bonuses tied to formulary compliance and prescription volume—what drugs your employees use and how often. Stop-loss carriers may pay performance bonuses tied to claims management or retention. These payments are rarely disclosed, even though they can materially affect what you end up paying for drugs and coverage.

In these arrangements, consultants are supposed to be negotiating contracts on your behalf. Instead, they may be getting paid by the same vendors you’re trying to negotiate against.

Trips, dinners, and appreciation events

Not all compensation shows up as a check. Carriers fly consultants to conferences in resort locations. They host dinners at steakhouses. They send gift baskets, tickets to games, and invitations to exclusive events. Individually, these perks may seem minor compared to six-figure commission checks.

While many companies have conflict-of-interest rules for vendors that may apply to you, they don’t apply to your benefit consultants. Over time, these perks build loyalty to certain carriers and vendors. And that makes it harder for a consultant to walk away or recommend you do the same.

“Free” technology that isn’t free

Many consultants offer benefits administration platforms at little or no cost. Enrollment tools, eligibility tracking, and employee portals are all included as part of the service.

Sounds great, right? Except someone has to pay for that technology. In many cases, carriers and vendors subsidize the platform in exchange for your consultant steering business their way. You’re paying for it through steered vendor selection and limited options.

Once you’re using the platform, switching becomes a hassle because your data lives there, your employees are trained on it, and your HR team has built workflows around it. The harder it is to leave, the easier it is for consultants to keep you with the vendors funding the technology, regardless of whether those vendors are the best fit for your plan or not.

Why this matters to employers

Under the Employee Retirement Income Security Act (ERISA), you have a fiduciary duty to act in your employees’ best interests when making benefits decisions. If you’re taking advice from someone with undisclosed financial conflicts, you’re not meeting that duty, and courts are paying attention.

“We didn’t know” isn’t a defense anymore. Employers who fail to demand transparency are increasingly being held liable for breaching their fiduciary obligations. The penalties are real.