Are You Getting the Information You Deserve from Your Broker or Benefit Consultant?

Three-party systems are transparency killers.

When I first became personally and emotionally invested in fixing America’s healthcare system, I zeroed in on a core dysfunction: the three-party structure involving payers, providers, and patients. This setup, while seemingly balanced, often obscures accountability and undermines transparency.

To understand what makes an economy function effectively, I turned to economic research. The fundamentals are surprisingly simple. A healthy market requires:

A system of price discovery – so all parties can agree on a fair price.

A lack of monopolistic behavior – to ensure competition.

Ease of market entry and exit – to foster innovation and entrepreneurship.

Of these, I focused on price discovery. There are several mechanisms for it—negotiation, bidding, and transparency. In a three-party system, however, only one method ensures fairness: full transparency. When three parties are involved, and all must operate with the same information, that information must be openly accessible to all. Anything less invites imbalance.

I once told the President of the United States: “Price transparency won’t fix everything, but nothing can be fixed without it.”

That conversation helped lead to a presidential executive order, now known as the Transparency-in-Coverage rules.

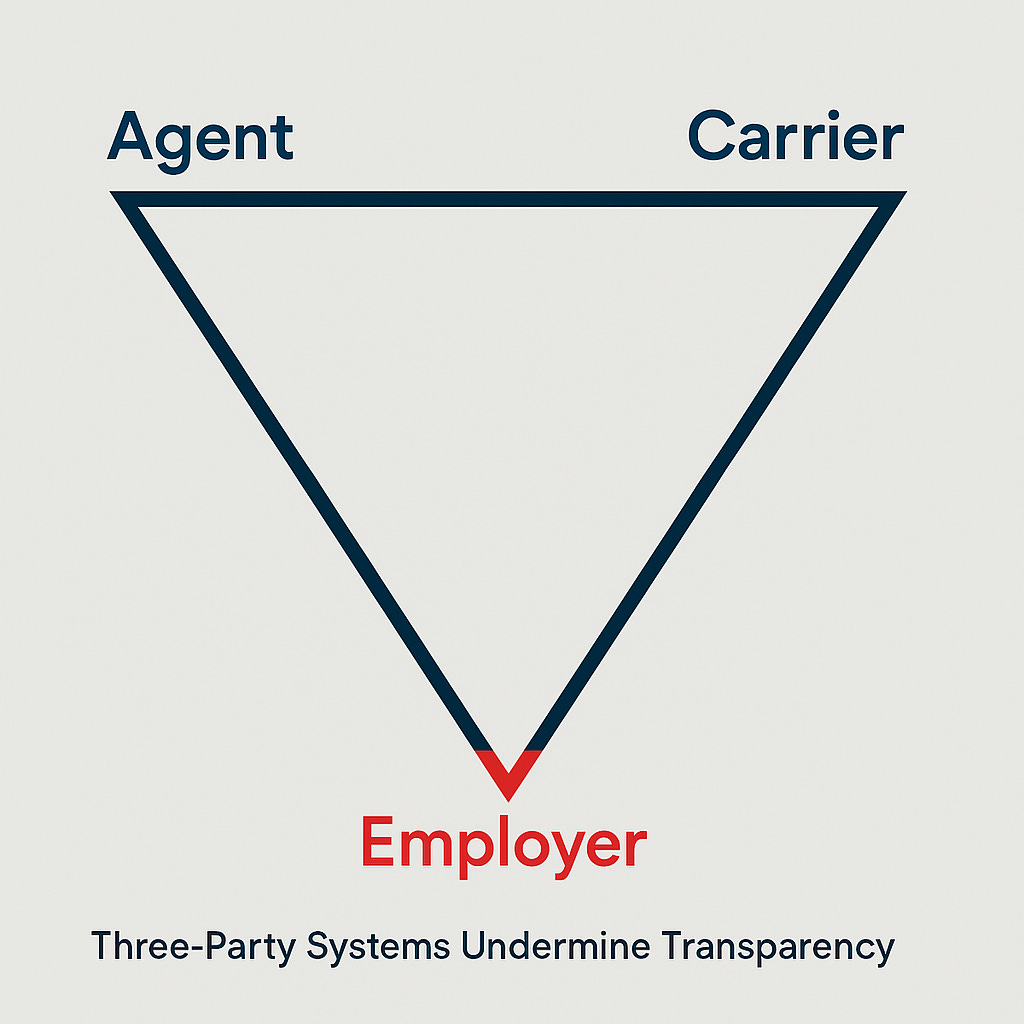

But healthcare isn’t the only area where three-party systems obscure the truth. Consider how employers purchase medical insurance. Here, the three parties are the employer, the insurance agent, and the insurance carrier. In this triangle, the employer—like the patient in the healthcare model—is often left in the dark.

When transparency is lacking, collusion between any two parties can dominate the system. In healthcare, payers and providers employ entire teams to “enhance the revenue cycle” and maximize profits—while patients navigate the system alone. In the insurance market, it’s often carriers and agents who align their interests, leaving employers exposed.

In 2021, a new law took effect requiring transparency in these employer-agent-carrier relationships. Yet compliance remains low. Many agencies only provide the required disclosures if clients explicitly ask for them.

For self-insured employers, this is especially critical. Under ERISA, they are fiduciaries of their medical plans. That means they are legally responsible for managing those plans in the best interest of their employees. Without full transparency, they risk making poor decisions—and facing lawsuits.

Major corporations like JPMorgan Chase, Wells Fargo, and Johnson & Johnson have already been sued by employees for breaching their fiduciary duties related to healthcare plans.

The law is clear. Employers must demand transparency. If you’re a self-insured employer, you can use the template below to request the required disclosures. Without them, you’re just as vulnerable as your employees—trapped in a three-party system where opacity breeds exploitation.

Your Company Letterhead]

[Date]

[Consultant/Broker Name]

[Consulting Firm Name]

[Address]

[City, State, ZIP]

Subject: Request for Full Disclosure of Compensation in Accordance with the Consolidated Appropriations Act, 2021

Dear [Consultant/Broker Name],

As the fiduciary of our employee group health plan, and in accordance with Section 202 of the Consolidated Appropriations Act (CAA) of 2021, we are writing to formally request a comprehensive disclosure of all compensation you or your firm expect to receive in connection with the services provided to our plan.

Specifically, please provide the following information in writing, no later than [insert reasonable deadline, e.g., 10 days from the date of this letter]:

Description of Services: A detailed description of all services you will provide to our group health plan, including any services provided by affiliates or subcontractors.

Direct Compensation: A breakdown of all direct compensation you expect to receive from our plan, either in aggregate or by service. This includes flat fees, per capita charges, or percentage-based fees. Please include all services you procure directly for us, including insurance products, ancillary services, and administrative systems (e.g., enrollment platforms, compliance services). This includes all aspects of insurance, from network access to stoploss and wrap networks.

Please be sure to exclude nothing, regardless of any language that may appear in any contract. The law and disclosure requirements override any confidentiality clauses in contracts you might have with third-parties.

Indirect Compensation: A description of all indirect compensation expected from third parties (e.g., insurance carriers, vendors), including:

The payer of the compensation

The services triggering the compensation

The arrangement under which the compensation is paid

Any contingent or formula-based compensation (e.g., bonuses, overrides, persistency incentives)

Transaction-Based Compensation: Any commissions, finder’s fees, or similar incentives, including the payer and recipient of such compensation.

Termination Compensation: Any compensation expected in connection with the termination of our agreement, and how any prepaid amounts will be calculated and refunded.

Estimates and Methodologies: Where exact amounts are not known, please provide good faith estimates, including the methodology and assumptions used to calculate them.

Please note that failure to provide this disclosure may render our agreement non-compliant under ERISA and subject to penalties. If you have already prepared a disclosure document that meets these requirements, please forward it to us at your earliest convenience.

We appreciate your cooperation in helping us fulfill our fiduciary responsibilities and ensure compliance with federal law.

Sincerely,

[Your Name]

[Your Title]

[Company Name]

[Email Address]

[Phone Number]