The Cavalry Isn't Coming

No one is going to reduce your healthcare spend except you.

Every year, the renewal arrives with a massive, double-digit increase. The CFO grumbles, the HR director panics, and your broker sits across the table, apologizes, blames “the market,” and the dance begins.

They say they’ll go back to the carrier to “see what they can do.” They shuffle some numbers around, raise the deductible a bit, and maybe pitch you a shiny new app to help manage chronic conditions or reduce emergency room visits. Exhausted and out of time, you reluctantly sign the contract. You accept the pain because you believe you have no other choice.

If you are sitting in the C-suite waiting for your broker, your benefit consultant, or a politician in Washington to swoop in and drive down your healthcare costs, you are going to be waiting until your balance sheet bleeds out. The cavalry is not coming.

It is time to face the reality of the people you are trusting to manage your supply chain.

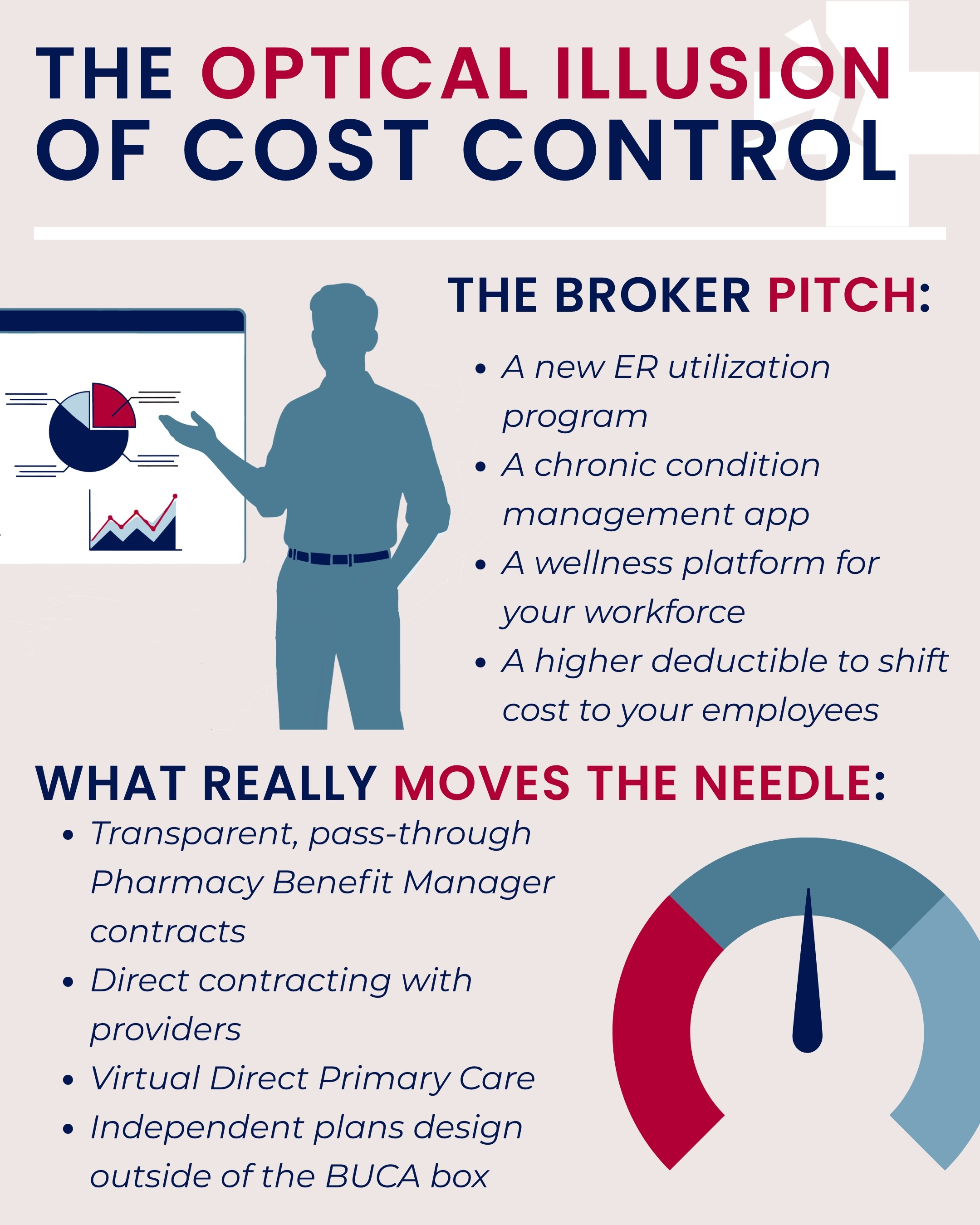

The optical illusion of cost control

Under the legacy system, attempting to control costs has become nothing more than a game.

Your traditional broker has to show that they are making an effort to justify their existence. But because the core medical networks they sell are essentially identical commodities, they can’t actually negotiate the price of your care. So, they pitch “innovative” point solutions. They boast about tackling emergency room utilization or sending your diabetic employees through a new management portal.

Let’s call this exactly what it is: an optical illusion.

There is virtually nothing they can do to move the financial needle from inside the legacy box. Tinkering with ER visits doesn’t stop a massive regional hospital from charging you $4,000 for a routine MRI that costs $400 down the street. A wellness app does absolutely nothing to stop a Pharmacy Benefit Manager (PBM) from extracting a massive spread-pricing markup on a generic pill.

They are showing you effort, but the effort is entirely misdirected.

Ignorance or negligence?

So why don’t they pull the levers that work?

It is easy to take the cynical view. We know the legacy brokerage compensation model is fundamentally rigged. When your advisor is paid through percentage-based commissions, hidden backend overrides, and volume bonuses from the supply chain, they aren’t working for you. They are operating as an outsourced sales force for the legacy carriers. They are financially penalized for saving you money and rewarded for driving up your costs.

But there is a less cynical, and perhaps much sadder, view.

The truth is that many traditional brokers simply do not know how to fix your plan. They have not become students of the system. They don’t understand the underlying plumbing. They are not masters of alternative plan design, transparent pass-through PBMs, direct contracting, or Virtual Direct Primary Care.

And in their defense, few of them are familiar with the details of how deep the PBM shell games really go. They just rely on the carrier to do the thinking for them. Benefit consultants who put all of their clients into bundled, off-the-shelf BUCA (Blue Cross, United, Cigna, Aetna) Administrative Services Only models may not be intentional thieves, but at a minimum, they are guilty of extreme negligence.

The levers are jammed

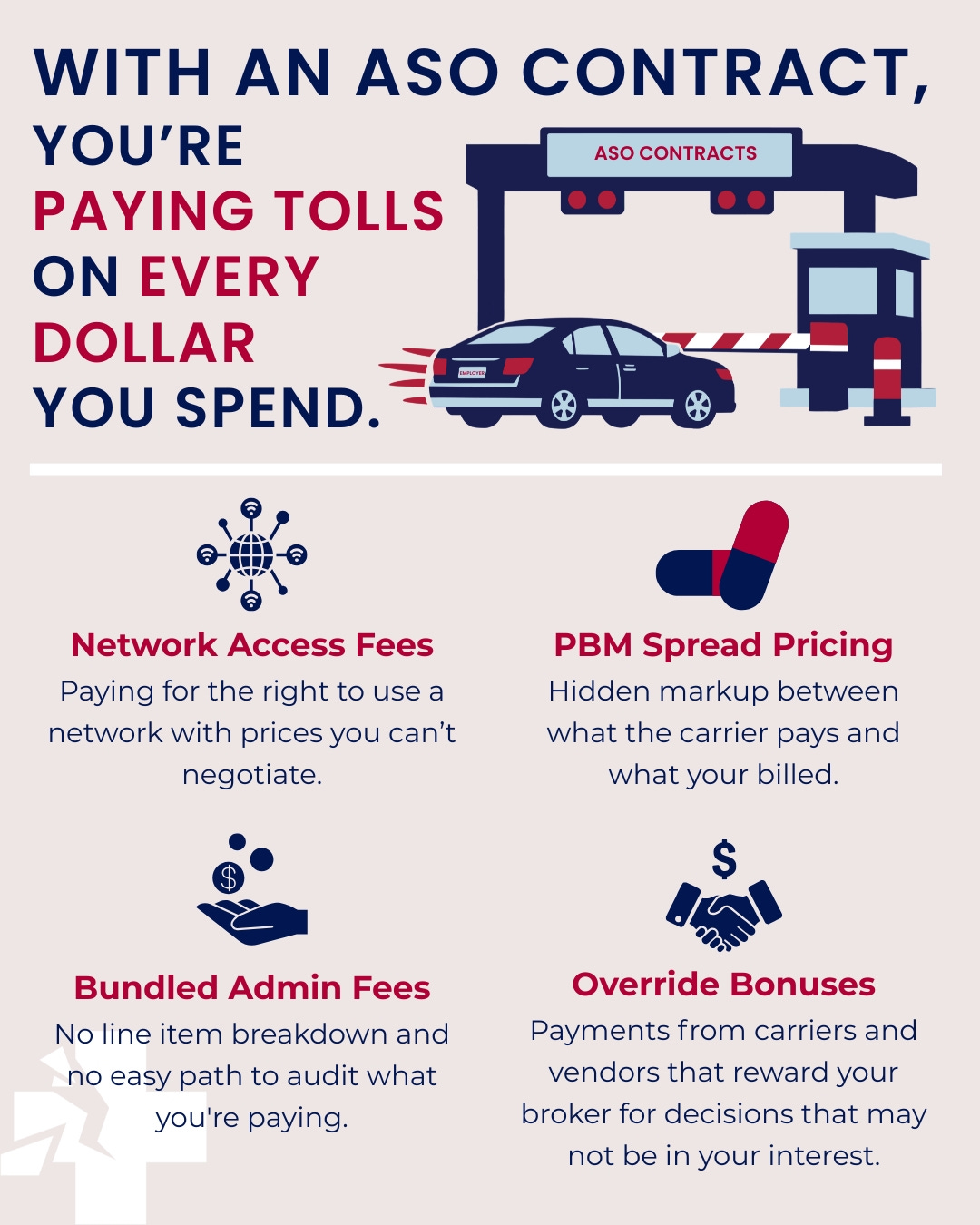

Even if your broker suddenly woke up tomorrow and wanted to fix your plan, the legacy system has completely jammed the levers required to do it.

When you purchase a bundled ASO plan from a legacy carrier, you are not buying a health plan; you are committing to paying a neverending fees to their a carrier’s administrativea tollbooth. You are surrendering to a system of fees you don’t understand, fees you don’t choose, and fees you don’t control.

To reduce your healthcare spend, you must demand the same procurement freedom for your health plan that you demand for every other operational spend in your business. You would never hire a Chief Procurement Officer for your manufacturing line and then legally forbid them from negotiating the cost of raw materials. But as long as you are locked inside a BUCA contract, you are forbidden from sourcing cheaper international specialty drugs, bypassing the PBM cartel, or paying a local independent doctor a fair cash price.

Choose your ecosystem

Your benefit consultant is not going to voluntarily disrupt their own revenue stream to build you a transparent, independent operating system. They are not going to change your plan design unless you insist on it. Frankly, they won’t insist on it themselves unless they know they will lose your business if they don’t.

The traditional strategy of acting as a passive buyer is a death sentence. You have to choose your ecosystem.

You must transition from being a passive buyer of an off-the-shelf insurance product to the active owner of a customized healthcare plan. You must redefine your broker as a fiduciary, fee-based advisor who sits entirely on your side of the ledger.

Your legacy carrier is not going to innovate its way out of their own profits. If we are going to dismantle the 50% administrative waste crushing the American economy, the mandate must come from the ground up.

Employers are the only ones with the power, the capital, and the fiduciary imperative to act. Employers are the only ones who are going to save employers.