ICHRAs: Think Before You Leap

What ICHRAs really do to your costs, your workforce, and your ability to fix either.

Double-digit increases in healthcare costs have become the norm for small and mid-sized companies. One-third of mid-size and large employers absorbed double-digit rate increases in 2026, exceeding the general inflation rate by 3x. Many leadership teams are flipping out. A 10% increase is a heavy hit to the P&L, but when that increase compounds year after year, it begins to look like an impending crisis.

The result is a sense of helplessness and, in some cases, fear.

Fear is a powerful motivator, and it is one that can easily be abused. Desperate to find solutions to appease their clients, many benefits brokers have started aggressively pointing employers toward Individual Coverage Health Reimbursement Arrangements (ICHRAs).

The rationale is simple. Brokers can’t do nothing because they need to get credit for doing something. Even if that something really amounts to nothing at all.

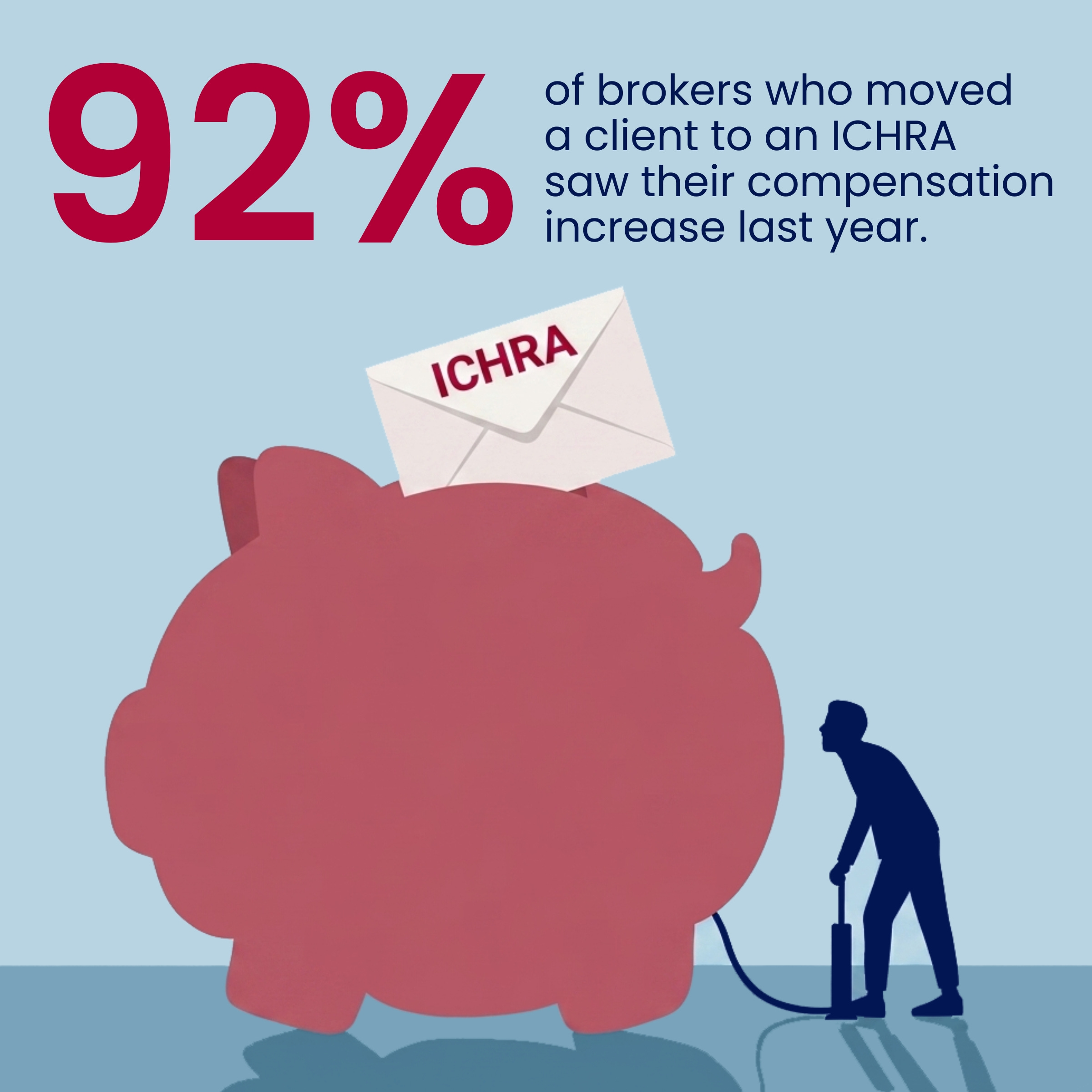

Cycling health plans works, and it pays. In 2025, 92% of brokers who moved clients to an ICHRA saw their compensation increase. That compares to 64% in 2025.

But ICHRAs are not a solution to employers’ healthcare woes. They are a white flag. There is no viable, long-term solution for employers other than to self-fund, take control of their supply chain, and actively manage their exposure.

Here is why the ICHRA is an illusion, and why it ultimately fails both employers and their workforces.

1. ICHRAs do nothing to address rising costs

The fundamental premise of an ICHRA is a sleight of hand. It converts a defined health benefit into a defined financial contribution. You set a budget, hand your employees a stipend, and send them to the individual marketplace.

ICHRAs do nothing to address the underlying drivers of healthcare inflation. They don’t strip out administrative bloat, they don’t bypass opaque Pharmacy Benefit Managers (PBMs), and they certainly don’t challenge the hyper-inflated billing practices of consolidated hospital systems. The cost of healthcare remains the same, the ICHRA simply caps the employer’s exposure to it.

Meanwhile, the cost of individual marketplace plans is skyrocketing right alongside fully-insured group plans, offering only a temporary and superficial reprieve to employers. And then… they are locked in.

2. ICHRAs create adverse selection and an affordability trap

It is vital to look at who is moving to ICHRAs. It is the companies with the absolute highest healthcare costs that are most desperate for an exit ramp, and they are the ones flocking to the false sense of safety that ICHRAs provide. This inherently injects massive adverse selection into the individual market risk pools.

Furthermore, employers cannot pretend the cost problem goes away just because they have capped their contribution. The ACA affordability requirements still stand. When a company moves to an ICHRA, they might see a small, temporary reset in their baseline by capping their initial costs. But as the adverse-selection-heavy individual market experiences double-digit premium spikes, the employer’s required contribution to remain compliant will surge right alongside it. You aren’t escaping the compounding increases; you are just delaying them by a cycle or two.

3. ICHRAs represent the ultimate in cost-shifting to employees

If the employer’s contribution is capped (or trailing the market) and the underlying cost of healthcare continues to surge, who absorbs the inflation? Your employees do.

The industry likes to dress this up as “empowering employee choice,” but the reality is much darker. When individual market rates spiked by an average of over 21% in 2026, employees on ICHRAs were forced to buy down into narrower networks and higher-deductible tiers just to afford coverage. The human toll is already visible in the data: currently, 39% of employees report delaying medical care because of cost. Pushing your workforce into a volatile, destabilized risk pool where they are exposed to extreme annual rate hikes hollows out the core value of the benefit you are paying for.

4. ICHRAs do not promote competition in the individual marketplace

The promise of an ICHRA relies on a robust, competitive individual marketplace where carriers fight for consumer dollars, driving down prices and increasing quality. That marketplace does not exist.

With the expiration of the enhanced ACA premium tax credits, the individual market has become incredibly volatile. Major carriers routinely exit markets where the risk pools become unprofitable, leaving consumers with a shrinking list of options. Instead of driving competition, ICHRAs simply feed more lives into an unstable, heavily consolidated system where employees lack the collective purchasing power to demand better rates or better care.

5. ICHRAs decouple risk from health plans

By retreating to the fully-insured individual market via an ICHRA, employers forfeit the most powerful levers they have to fix their healthcare. ACA marketplace plans are the ultimate fully-insured “black boxes.” They are subject to the oppressive, generalized requirements of the ACA and HIPAA that prevent you from actively managing your costs.

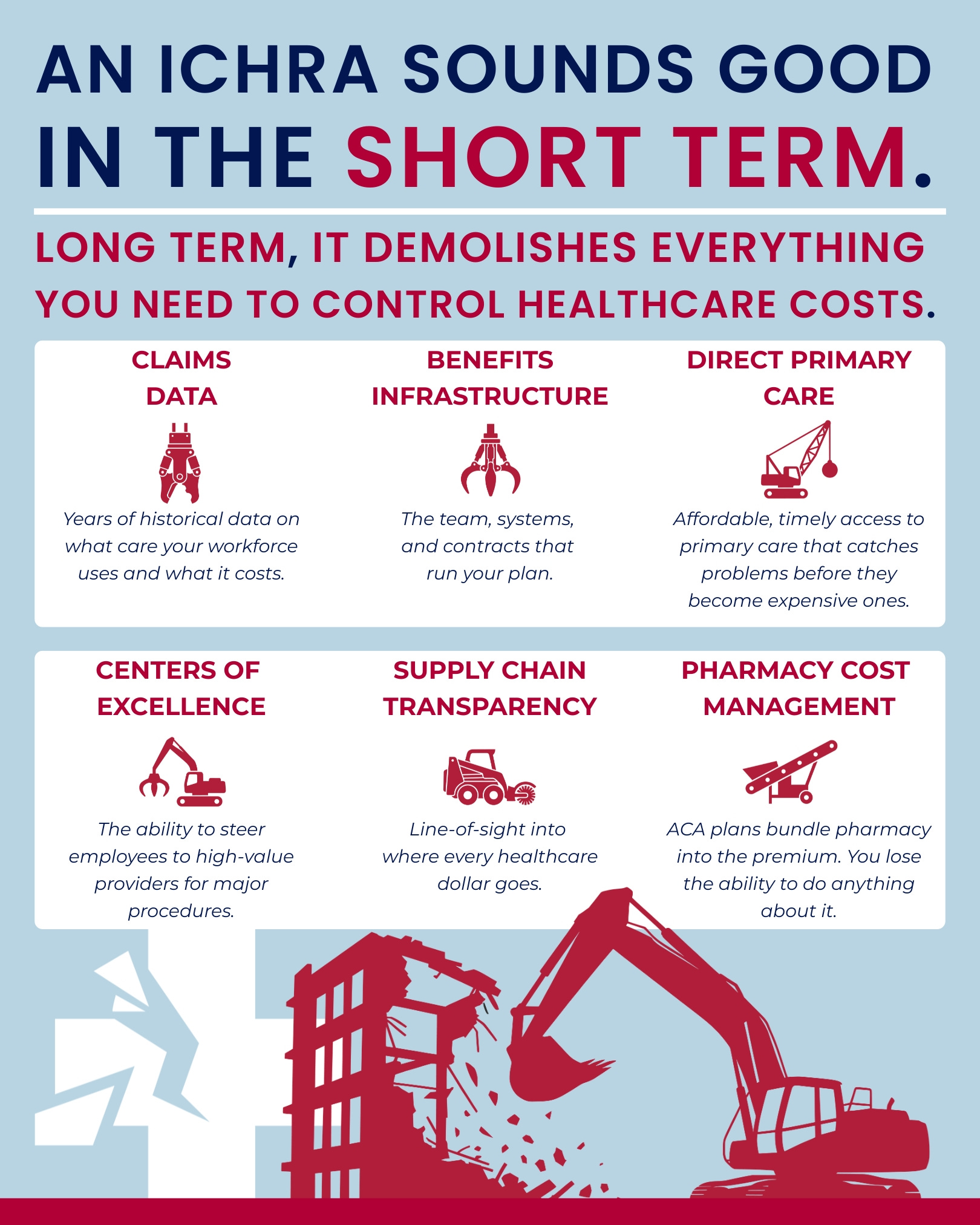

You cannot build a sustainable employer health strategy on an ICHRA. The moment you make the move, you give up the levers that enable you to manage costs — the localized claims data that lets you identify supply chain inefficiencies and apply AI to spot patterns, the ability to bypass traditional carrier networks, the power to carve out PBMs, the freedom to implement direct primary care, and the option to steer members to high-value centers of excellence.

6. ICHRAs are a "one-way” door

Eventually, the year-one savings will disappear and companies will see the ICHRA for what it was — a way to delay the problem, not solve it. They will need to bring healthcare back in-house to manage their costs and supply chain.

Giving up your current group plans for the ICHRA market makes transitioning back exponentially harder. You will have surrendered years of historical claims data, scattered your workforce across dozens of disconnected individual carriers, and completely dismantled your internal benefits infrastructure. You will be starting from scratch, from a position of total weakness.

A final note

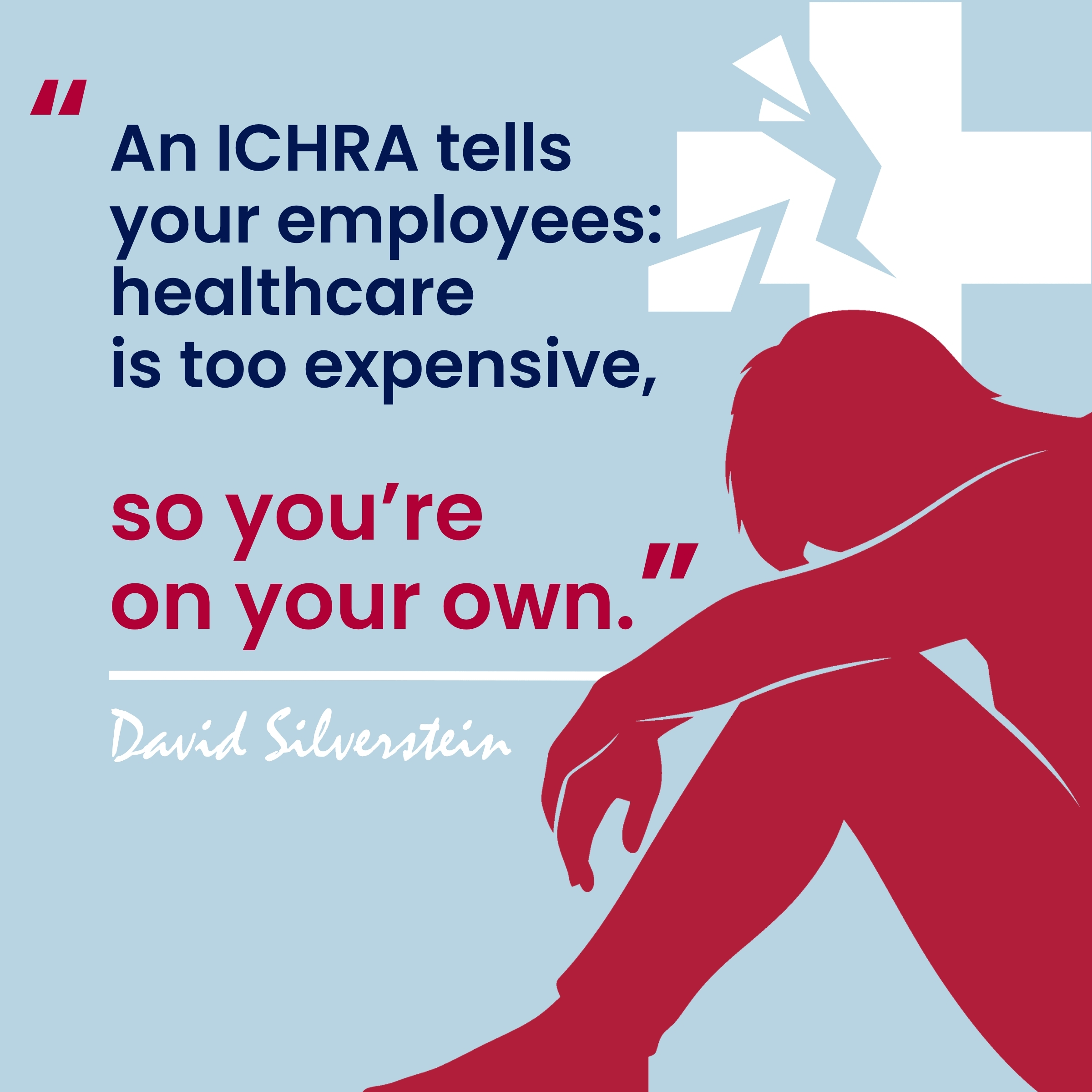

An ICHRA tells your employees, “Healthcare is too expensive, so you’re on your own.” A better approach tells your employees, “Healthcare is too expensive, so we built a better system.”

Financial predictability and high-quality care do not come from capping what you pay and walking away. They come from building a real health plan, one where you control the economics instead of surrendering them. Self-fund, demand transparency, and manage your supply chain. Everything else is an illusion.